{kind=link}

What Problems Does Your Solution Create?

Feb 24, 2014

Have you ever heard this phrase before? Theoretically, it must be true. Every time we address a problem and believe we have come to a resolution, it often creates another “problem” or “challenge”. It must work this way, or we would be dealing with perfection.

Have you ever heard this phrase before? Theoretically, it must be true. Every time we address a problem and believe we have come to a resolution, it often creates another “problem” or “challenge”. It must work this way, or we would be dealing with perfection.

I heard this from a client a few weeks ago, and it was really thought provoking. We spend endless hours every day solving problems, but are the solutions really the best and most efficient? Several weeks ago I had an opportunity to speak with a newly promoted CFO. She had been at the business for many years (10+) and her mentor, the former CFO, had recently retired and she was more than excited to take his place, but realized after just a few short weeks that maybe some of the way “things were being done” was not the most efficient and maybe not even correct.

For starters, her background was strictly financial and she felt she had very little capacity for managing product costing and pricing, as well as, management accounting aspects overall. As we began to talk, she asked how William Vaughan Company could help her understand this feature of her job and overall what services we could offer to her. I explained that I needed to gain a better understanding of what the business was doing now as far as operations, and spend some time doing a thorough review of the current cost model.

Unfortunately, as the conversation ensued, I discovered this business was like so many others. Over the years, as the system broke down, many aspects of the cost model had been hung together using extracted information from an underutilized system and manipulated into an overwhelming Excel spreadsheet that was not understood and most likely incorrect.

The problem? Initially someone did not understand the software, did not recognize the capabilities of the software, or just decided to start an excel spreadsheet.

The solution? Going around the system to create a tool that used to manage profitability of the Company. However, now it created a new problem. We have identified that the system is not capable of performing tasks and we made the decision to continue to work “outside” of the system.

The solution? Continued use of spreadsheets, under-utilization of the system, and increasing risk for errors and lack of data integrity.

I could go on, but it is a pattern I see more often than not. This blog is interesting, because it blames the problem on the business, not the individuals who first made the decision.

While I am certainly not advocating these tools, Mr. Sommer does a good job of describing “spreadsheet addicts”– almost worth reading just for a laugh.

You are likely in the majority, and over utilizing spreadsheets and underutilizing your system whether for traditional accounting transactions or product costing. Speaking from experience, if you step out of your comfort zone and make the change, you will see that the effort will bring with it great results.

Categories: Cost Accounting

Categories: Cost Accounting

Least Squared Method: A Guide to Break-Even Points

Feb 20, 2014

Are you familiar with the Least Squared Method, or as some may call it, the Method of Least Squares. If so, it was probably in a statics class in college, or maybe it is a tool you frequently use. If not, simply put, it is a technique used to determine the line of best fit to data. The calculations are a dizzying series of calculus and algebraic formulas. Fortunately, Excel has a program to calculate the Least Squared Method. The thought of estimating true values and averaging out errors of increases an decreases actually was first expressed in 1722 by Roger Cotes, who was an English Mathematician, who worked closely with Sir Isaac Newton. As you can see this is not a new thought, but perhaps a new way of thinking…

One way we use the Least Squared Method is to compare a series of break-even points over time. Most recently, a client came to me saying they needed their break-even point down. Of course that leads to a discussion on how to do that. We talked about trying to limit spending as much as possible on some of the simple things like office supplies, or purchasing new office equipment, etc. We also talked about more difficult things like minimizing scrap, improving processes, etc. Many times owners find out that if they really watch and they push hard enough, especially in production, they can decrease their break-even point and hopefully get through and eventually flourish.

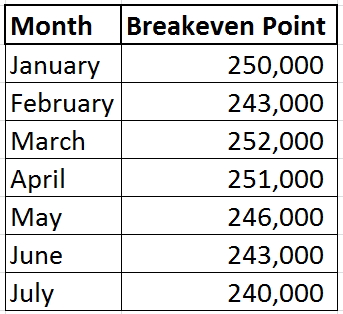

There will be months were the break-even point decreases dramatically and then months where it is higher than when you first started making efforts to decrease it. Although looking at the break-even point month-by-month is quite important, it may lose some meaning if you do not look at it using the Least Squared Method. You may feel quite discouraged when the break-even increases in a given month, but if you looked at it in whole, you would clearly see it has actually been a steady decrease. This statistical method is an easy tool that helps you see that. For example, the table below lists break-even points for January-July of any given year.

You can see in the table above that the break-even point fluctuates month-to-month, however, in the chart below you can see the Least Squared Method trend line shows that the overall trend is decreasing.

Without the simple use of this statistical tool you may end up frustrated looking at the numbers month-to-month thinking things are not improving the way you want and need them to, but from this chart you can see you are going in the right direction.

Categories: Cost Accounting

Managing Costs for a Healthier Bottom Line

Feb 20, 2014

Your company’s profitability depends not only on sales, but also on effective cost management. Are you adequately addressing the cost side of the business equation?

Your company’s profitability depends not only on sales, but also on effective cost management. Are you adequately addressing the cost side of the business equation?

Analyze Your Cost Structure. You probably can readily identify the products and/or services that are generating your greatest sales volume. But can you identify all the costs associated with providing each product or service? Only when you know your true costs can you effectively allocate resources to the work that is most profitable for your company.

Actively Monitor Operations. As the busy owner of a small business, you can’t be everywhere all the time. But you do need to stay in circulation, regularly observing the day-to-day operations of your business and talking to your managers and employees. By staying visible and encouraging an open dialogue, you’ll be in a better position to uncover costly problems before they seriously erode your company’s bottom line.

Solicit Bids. Even if you are satisfied with a current vendor, you may want to talk to the competition from time to time. You won’t necessarily want to switch vendors simply because you are quoted a better price. But you may be able to use that price in negotiating more favorable terms from your existing supplier.

Watch for Discounts. In the interests of cash flow, your company may routinely pay its bills only when they come due. While this generally is a sensible strategy, it may not be wise if you are passing up generous cash discounts for earlier payment. In the current low interest rate environment, borrowing the funds you need to take advantage of discounts may be a better move. For example, suppose a vendor offers your company a 2% discount for paying a $10,000 invoice 20 days early. Passing up the discount will cost you $200. Instead, you might borrow $9,800 from your bank, pay the discounted invoice, and repay the loan in 20 days. If the rate on your bank line of credit is 8%, you’ll owe about $45 of interest — for a net savings of $155 on just one invoice.

Effective cost management requires good information and careful planning. Our team of costing accounting experts can help you identify your pitfalls and help you clarify yours costing system.

Categories: Cost Accounting, Manufacturing & Distribution

Change In Product Volume & How to Handle the Situation

Feb 17, 2014

Recently I was talking to a client concerning some dramatic changes in their volume and how product costing might affect which jobs they take in the future. In this case, the client had been operating at a comfortable volume and was profitable every month with more than enough activity to keep his entire operation busy. Due to some changes with one customer, a substantial portion of his volume was lost and now he is left with activity levels well below his break-even point. His first thought was to reduce his overhead as much as possible in order to reduce his break-even point. Of course this is always a good idea, but in his case, not nearly enough overhead could be removed to make operations profitable or even break-even at the volumes he was anticipating.

Recently I was talking to a client concerning some dramatic changes in their volume and how product costing might affect which jobs they take in the future. In this case, the client had been operating at a comfortable volume and was profitable every month with more than enough activity to keep his entire operation busy. Due to some changes with one customer, a substantial portion of his volume was lost and now he is left with activity levels well below his break-even point. His first thought was to reduce his overhead as much as possible in order to reduce his break-even point. Of course this is always a good idea, but in his case, not nearly enough overhead could be removed to make operations profitable or even break-even at the volumes he was anticipating.

Shortly after all these changes in his volume, he received an opportunity to take on another job. This new job was the topic of our conversation. The new job was offered at a target price with the commitment that if he could meet the target price, he could have the job. The problem, however, was that the gross margin on this job would be in the neighborhood of 15%. That means that the direct cost of producing the job would leave a margin that contributed only 15 cents on each dollar of sales to overhead and profits. The question before us was, should he take the job.

I am sure most cost managers at some time in their career are faced with a similar question. Should the company accept a job with margins that are substantially below historical margins? And, what would be needed to cover general and administrative cost, as well as, profitability?

My typical answer in circumstances like this is: it depends. It depends on the overall profitability of the company, it depends on other activity related to current sales volume that’s happening in the company, it depends on the duration of the job as well as the technical complexity of the job and the likelihood that the quoted costs to get the job will really be how those costs play out in actual production.

In this case, I would recommend that the president take this job and contribute that very small amount of profit to overhead rather than continuing to struggle with no activity and no contribution to his overhead which would likely be the case without taking this job. That advice would be predicated on the fact that we have history with the customer and they have been reliable as far as paying within terms, and in overall business. I think it may be able to get him close to break-even, or at least improve cash flows.

Categories: Cost Accounting

The BIG Picture: Break-even Analysis

Feb 13, 2014

Break-even analysis can be and certainly is used characteristically to do just that, determine the break-even point for a business. This is usually looked at in a total fashion, something like I need to have $150,000 in sales each month to break-even. It is usually pretty straight forward and is easy to understand which is why many business owners apply such thought process. It also can be a very valuable analytical tool, meaning, if you do not believe you will have those kinds of sales in the coming month, you can take action to try to increase your sales and/or decrease your costs. If you do not know your break-even point and you go into the month blind, you cannot be proactive, only reactive, which after many months of being below break-even you may be in a situation in which it will be difficult to recover.

Break-even analysis can be and certainly is used characteristically to do just that, determine the break-even point for a business. This is usually looked at in a total fashion, something like I need to have $150,000 in sales each month to break-even. It is usually pretty straight forward and is easy to understand which is why many business owners apply such thought process. It also can be a very valuable analytical tool, meaning, if you do not believe you will have those kinds of sales in the coming month, you can take action to try to increase your sales and/or decrease your costs. If you do not know your break-even point and you go into the month blind, you cannot be proactive, only reactive, which after many months of being below break-even you may be in a situation in which it will be difficult to recover.

A more non-traditional application for a break-even point is using the calculation to help determine if an additional capital expenditure is worthwhile. You may be thinking of purchasing a new piece of equipment which is typically a larger investment than your everyday expenses. As a result, this requires more methodical decision making techniques to determine its benefit, it any. Break-even can be one of those techniques. Typically the reason for purchasing a new piece of equipment is to reduce your variable costs. However, it will increase your fixed costs, such as interest and depreciation. I the decrease in variable costs is not more than the extra in fixed costs, it most likely is not a viable investment. Your break-even point should go down with a new piece of equipment!

There are some important things that need to be known in order to do this calculation! You need to know what the fixed costs for this piece of equipment are going to be, what the new variable costs will be, and of course, what the sales associated with it will be. These are all the necessary parts of a break-even analysis. It all seems simple enough, but if you are looking to purchase this machine, you do not yet have it to know these things for certain. It is important to do as much research and have as much valuable information as possible. Keep in mind the dealership selling the equipment wants to make a sale and may inflate some of the positive numbers, and will be supplying you with averages that you may be on the low end or high end of. Nevertheless, this can be a very valuable tool in determining if it is a viable option. If your sales will have to be so high to cover the costs of a new machine, then it may not be worth it.

Like all calculations it is vital to have good general ledger numbers you are using to compare and understand the changes this new equipment will present. Also do not get hung up at only looking at one side, like just the expense side, but also at the big picture. Break-even analysis is that big picture.

Categories: Cost Accounting