{kind=link}

Determining Your Infectious Disease Risk During the COVID-19 Outbreak

Mar 18, 2020

Provided By BDO Alliance, USA

A Checklist for Organizational Leaders

On March 11, the World Health Organization (WHO) declared the novel coronavirus (COVID-19) outbreak a pandemic, with numerous countries—including China, the Czech Republic, Hong Kong, Italy, Slovakia and the U.S.—announcing travel restrictions and social distancing measures.

Beyond the immense impacts the outbreak is having on public health, the pandemic directly impacts economic activity and poses unique challenges to businesses across industries because of its potentially compounding and unpredictable consequences.

With massive quarantines, travel restrictions and factory shutdowns, companies are struggling to quantify potential exposure. Attempting to mitigate potential losses from an unknown number of variables is daunting, especially when the situation is changing daily. Business owners and risk managers will face not only tactical execution and recovery challenges, but also the prospect of navigating a lengthy insurance claim process.

Understanding how to determine and capture lost revenue and income stemming from this unpredictable outbreak is critical to minimize financial implications. To do that, business leaders must determine their infectious disease risk profile:

Here are the key questions organizational leaders need to ask to evaluate their risk profile and the corresponding action items to navigate the ongoing outbreak:

1) How prepared is my organization? What does “prepared” look like to our organization?

- Conduct a business continuity risk assessment to identify potential internal operational, financial and market risks; determine direct and indirect impacts; and generate an action plan. Third-party vulnerabilities should be incorporated into action plans.

- Identify a response team to lead ongoing crisis management efforts, coordinating with appropriate federal, state and local authorities. These efforts should include regular communication to internal and external stakeholders.

- Communicate with internal and external stakeholders—as well as their surrounding communities—about what coronavirus is and key protective measures people can employ. Leveraging information from WHO’s dedicated public advice page is a good place to start.

2) What are our organization’s capabilities, strengths and weaknesses, including across the supply chain? Which third-party risks do we have, and where are they concentrated?

- Build scenario models to determine ways to mitigate any additional risks to your supply chain, working closely with your suppliers.

- Insulate your supply chain from disruption. Identify ways to diversify your supply chain if possible and assess the cost-benefit of maintaining duplicate facilities or routes on an ongoing basis.

- Create a backup plan. Identify alternate sources should your primary source of supply be unable to deliver on services.

3) Have we clearly communicated to our workforce what steps they should take and how they should respond to different scenarios identified?

- Evaluate work-from-home arrangements and options for remote meetings and videoconferencing. Employees working remotely, meanwhile, will need secure remote access to necessary files and services, likely using a VPN, as well as collaboration tools including instant-messaging apps, project management platforms and shared documents.

- Review remote working policies and guidelines. Remote workers should only use their work computers and not their personal computers, and managers should be trained on how to be virtual leaders by setting clear expectations and emphasizing regular communication.

- Review policies for paid time off, sick leave and short-term disability. Employees should be reassured that they will not be penalized for taking sick leave, and they should not come into the workplace while sick because they are worried about losing out on income. Policies for payment if the workplace is temporarily closed or employees are furloughed will also need to be reviewed and clarified.

4) What is our organization’s insurance coverage, and do we have funds to support this crisis? Does your organization have coverage for an insurance claim?

- Evaluate your insurance coverage for business interruptions. Identify the impact from civil authority and ingress/egress coverage, service interruption, supply chain interruptions, loss mitigation, and extra expenses like increased logistics and redistribution costs, higher costs related to workforce disruption as well as shifting productions to potentially higher-cost locations, and others.

- Establish milestones for claim recovery. Resources are likely going to be stretched thin for the foreseeable future. It is important to create milestones and hold all members — from the adjusting team to internal stakeholders — accountable for achieving those goals.

5) How can this threat unfold and evolve, and what scenarios do we need to consider for our organization?

- Regularly monitor announcements from the WHO and the Centers for Disease Control and Prevention to determine other potential impacts that could be coming down the pike for your organization.

- Establish various versions of your enterprise risk plan that can be adapted to help mitigate risk should other waves of the outbreak take place, taking into consideration where they might unfold.

- Consider accounting implications and total tax liability changes. For example, COVID-19 could complicate how businesses comply with Current Expected Credit Losses (CECL) accounting given the complication to forecasting credit losses. Total tax liability, meanwhile, could be impacted in several ways depending on individual circumstances and the actions taken by national and local governments.

Following this checklist can better enable you to make informed operational and strategic decisions while balancing the risks inherent to an infectious disease pandemic. Beyond that, you can use the intel gained from your self-evaluation to build your capabilities over time and support the business case for future investments in resiliency.

Categories: Other Resources

Minimizing the Impact of Coronavirus (COVID-19) on Your Business

Mar 18, 2020

Amid the growing cases of coronavirus (CODVID-19), many state governments including Ohio and Michigan have instituted a mandatory shutdown of all bars and restaurants leaving many operators scrambling to figure out how to stay afloat. More recently, dental offices, spas, gyms and other businesses have been forced to close their doors to promote “social distancing.” Here are tips for staying healthy—and staying in business—during this unprecedented period:

Communication is Key

It is essential to communicate the latest information and advisories from your local state health departments to your team of employees. Make sure preventative measures such as sanitization, hand washing, and employee sick leave is conveyed and well understood. If your employees are able to work from home, remember to keep open lines of communication—check in regularly and communicate frequently; this applies to both the client and internal team members.

Many owners are communicating reassuring messages to their customers, providing confidence in their understanding of the severity of the virus. Make sure your customers know you are taking the proper steps to maintain a healthy work environment to protect not only your employees but your consumers as well.

Apply for a Small Business Loan

The SBA will work directly with state Governors to provide targeted, low-interest loans to small businesses and non-profits that have been severely impacted by the Coronavirus (COVID-19). The SBA’s Economic Injury Disaster Loan program provides small businesses with working capital loans of up to $2 million that can provide vital economic support to small businesses to help overcome the temporary loss of revenue they are experiencing. Find more information on the SBA’s Economic Injury Disaster Loans here.

Dust off your business continuity plan

The objective of the business continuity plan (BCP) is to help a business to efficiently return to normal activities after a major incident that directly affects operations. Items to consider, if not already done so include:

- Establish an Emergency Action Plan (EAP) and team

- Have the EAP team assess the situation and agree to an appropriate action plan based on demand, available supplies, and available labor

- Implement appropriate prevention methods and procedures to reduce risk

- Have management staff review and take appropriate action regarding sick-leave absences unique to a pandemic, including policies that define when a previously ill person is no longer infectious and can return to work

- Work closely with the local health department to monitor the situation and to deploy appropriate control measures

- Identify backups for each job position and alternate manufacturing sites in pandemic response planning

Shift your marketing strategy

Don’t stop marketing your business, instead now is the time to be creative. For example, if you are a restaurant, try to experiment with different third-party delivery providers or encourage customers to find any way to receive your product such as curbside pick-up. Compromised populations, such as senior citizens can benefit from meal delivery. If you have a restaurant app, consider providing a meal deal for a family. Thinking outside the box will ultimately help you stay afloat during this highly volatile time.

Categories: Other Resources

Unemployment Insurance Benefits For Those Affected By COVID-19

Mar 18, 2020

The impact of COVID-19 around the United States is understandably worrisome. We’re providing this information to you regarding the latest news from the Trump administration and the State of Ohio’s unemployment benefits if you find that you have furlough all or some of your employees.

The administration also has announced this morning that the IRS will be deferring IRS payments from individuals and pass-through entities. If you owe a payment to the IRS, you can defer up to $1 million as an individual or pass-through entities and up to $10 million to corporations, interest-free and penalty-free, for 90 days.

The administration continues to work on the economic stimulus plan with Senators and House of Representatives, including loan guarantees, payments to small businesses, and payments to the American workers. After passage, they are hoping that checks to individuals can be made immediately – in the next 2 weeks.

Please rely on official sources, press conference details from national, state and local authorities, as we are, instead of media reports. We will do our best to summarize the guidelines for our clients as we understand that interpreting the messages from the CDC and Ohio Department of Health can be daunting. Besides official press conferences, our two main sources are:

- National Centers for Disease Control – Guidance for Businesses

- Ohio Business Gateway – Message to Employers

Unemployment Insurance Benefits

COVID-19 Pandemic Unemployment Payment is a new social welfare payment for employees and self-employed people who are unemployed or who have their hours of work reduced during the COVID-19 (coronavirus) pandemic. This includes people who have been put on part-time or casual work. You can apply for the payment if you are aged between 18 and 66 and have lost employment due to the coronavirus restrictions. Students can apply for the payment.

Here’s what we know as of this writing about Ohio’s unemployment insurance benefits for your employees:

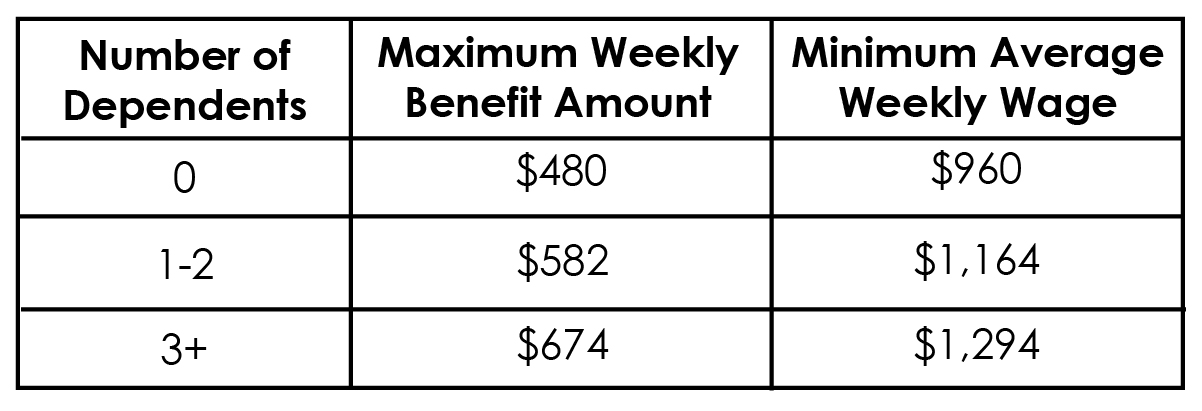

The weekly benefit amount is the amount of benefits employees may be entitled to receive for one week of total unemployment. Employees’ weekly benefit amount is computed at one-half of their average weekly wage during their base period (the base period is the 52 weeks prior to filing for unemployment). However, the weekly benefit amount cannot exceed the state’s annually established maximum levels (based on the number of allowable dependents claimed). The 2020 maximums for each dependency classification are given in the following table:

Example: $1200 average weekly wage X ½ = $600

Using this example, if an employee has 3 or more dependents, the weekly benefit amount would be $600 (as the maximum of $647 was not reached). However, if the employee had less than 3 dependents, the weekly benefit amount would be the maximum level allowable for fewer dependents (0 dependents = $480, while 1 or 2 dependents = $582).

NOTE: See below for information about deductible income and earnings which may reduce employee’s weekly benefit amount.

Employees must report all weekly income, including payments other than wages. In certain cases, the entire amount may be deducted from your benefits. Types of income that may be deductible include:

- Severance pay – Severance pay allocated by the employer to a week(s) following the date of separation is deductible from unemployment benefits.

- Vacation pay

- Pensions

- Company buy-out plans

- Workers’ Compensation

Employers can offer de minimis benefits (small amounts) like gift cards – generally under $75.

The waiting period of one week for unemployment benefits has been waived in Ohio. The Governor said employers will not be penalized for their employees filing for unemployment.

Filing for Unemployment Insurance Benefits

Ohio has two ways to file an application for Unemployment Insurance Benefits:

- Online – http://unemployment.ohio.gov – 24 hours/day, 7 days/week. Service may be limited during nightly system updating.

- Telephone – Call toll-free 1-877-644-6562 Monday through Friday 8 AM – 5 PM.

To apply for Unemployment Insurance Benefits, employees will need:

- Social Security number

- Driver’s license or state ID number

- Name, address, telephone number, and e-mail address

- Name, address, telephone number, and dates of employment with each employer worked for during the past 6 weeks of employment

- The reason why the worker has become unemployed from each employer

- Dependents’ names, Social Security numbers, and dates of birth

- If claiming dependents, their spouse’s name, Social Security number, and birth date

- Regular occupation and job skills – but employees will not have to actively search for jobs during this period.

- For your business and healthcare practices, there may be tax savings, low-interest loans through the SBA if other credit financing options are NOT available. The stimulus package being discussed is for individuals and certain small businesses under 500 employees.

Other Important Considerations

Business Interruption Insurance – Most businesses have, or should have business interruption insurance. You are urged to check with your business insurance broker to see if you have such coverage, determine if this qualifies, and what you need to do to receive reimbursement from your insurance company for your loss of business income. Up-to-date financial and payroll information will be critical.

Employment for dental workers – Healthcare workers are needed everywhere and it’s possible employees trained in HIPAA and other health safety precautions may be able to find work elsewhere. (Some requirements for HIPAA requirements have been waived for telehealth options.) Also, hospitals and medical centers are looking to dental offices to share the number of masks, gloves, etc., they have on hand.

As always, please call your William Vaughan Company advisor with any questions.

Categories: Other Resources