{kind=link}

Inflation Reduction Act Expands 179D (Energy Efficient Commercial Buildings Deduction)

Oct 17, 2022

The Inflation Reduction Act of 2022 (2022 IRA) was passed to incentivize investment in clean energy and promote the reduction of carbon emissions. A large share of the incentives come in the form of tax credits, which in some cases are extensions or expansions of current credits, such as those for electric vehicles or residential energy upgrades.

Of the tax provisions introduced by the 2022 IRA, one of the most significant to businesses has been the expansion of the Energy Efficient Commercial Buildings Deduction (§179D), which increases the maximum deduction and updates the eligibility requirements for a property’s reduction of energy costs, in addition to other changes.

Under the expanded provision, a deduction is allowed for all or part of the cost of certain energy-savings improvements made to domestic, commercial buildings placed in service as part of the building’s:

- interior lighting systems

- heating, cooling, ventilation (HVAC), and hot water systems

- building envelope

The tax deduction benefits both commercial building owners and lessees along with designers of government-owned buildings. Additionally, the provision states that installation of energy-efficient property may occur as a result of new construction, or through the improvement of an existing commercial or government building.

Efficiency standard: To qualify for the deduction, newly updated eligibility requirements call for energy-efficient property to reduce associated energy costs by 25% or more (decreased from 50% or more) in comparison to a reference building that meets the latest efficiency standards.

Applicable amount: The applicable dollar value of the deduction is $0.50 per square foot, an increase of $0.02 for each percentage point above 25% that a building’s total annual energy cost savings are increased. However the amount cannot be greater than $1/ square foot, and the maximum amount of the deduction in any tax year cannot exceed $1/ square foot minus the total deductions taken over the previous three years (or during a four-year period in cases where the deduction is allowable for someone other than the taxpayer). The applicable dollar value will be adjusted for inflation for tax years beginning after 2022.

An increased dollar value is available for projects that satisfy prevailing wage and apprenticeship requirements for the duration of the construction.

Alternative deduction for energy-efficient retrofit property. Under the 2022 Inflation Act, taxpayers may elect to take an alternative deduction for a qualified retrofit of any eligible property. However, instead of a reduction in total annual energy power costs, the deduction is based on the reduction of energy usage intensity.

For more information on how you may be able to take advantage of this deduction or any other tax relief provisions under the 2022 Inflation Act, contact William Vaughan Company’s team of trusted tax professionals.

Connect with us.

wvco.com

Categories: Tax Planning

The Affordable Care Act Survives Yet Another Supreme Court Challenge

Jun 22, 2021

Last week, the U.S. Supreme Court ruled once again on the constitutionality of the Affordable Care Act (ACA) rejecting arguments that the ACA was unconstitutional under Congress’ taxing power. Last year, the Supreme Court heard testimony in California v. Texas which focused on whether the ACA’s individual mandate to maintain health insurance was beyond Congress’s powers given that it no longer raises tax revenues and, if so, whether other parts of the law would need to be struck down along with the mandate. This case marked the third time the court had heard a significant challenge to the law.

Justice Stephen Breyer delivered the 7-2 opinion which stated the individuals that brought the lawsuit challenging the ACA’s individual mandate did not have the standing to challenge the law: “ we conclude the plaintiffs in this suit failed to show a concrete, particularized injury fairly traceable to the defendants’ conduct in enforcing the specific statutory provision they attack as unconstitutional,” wrote Breyer.

What does this mean?

The Supreme Court upheld the ACA, including its many tax provisions.

Protective claims

If you filed a protective claim in hopes the Supreme Court would rule the ACA, and its many tax provisions, retroactively unconstitutional, these protective claims are no longer valid. Protective claims are filed to preserve the taxpayer’s right to claim a refund when that right is contingent on future events and may not be determinable until after the statute of limitations expires.

If you have questions regarding your individual circumstance, please contact your William Vaughan Company representative or call our office at the number below.

Connect With Us.

wvco.com | 419.891.1040

Categories: Tax Compliance

Employers Can Provide Tax-Free Qualified Disaster Payments To Employees

Mar 24, 2020

Employers are scrambling to find ways to help their employees who are impacted by the novel coronavirus (COVID-19). Help is available. Now that the COVID-19 has been declared a national emergency,[1] Internal Revenue Code Section 139 can be used to allow employers to make tax-free payments or reimbursements to employees as “qualified disaster payments.” Below are some frequently asked questions about how employers can use Section 139 immediately to help employees cope with COVID-19.

Q1: What is a “qualified disaster payment”?

A1: Qualified disaster payments are payments that are not otherwise reimbursed by insurance made by an employer to an employee that are reasonably expected by the employer to:

- Reimburse or pay reasonable and necessary personal, family, living, or funeral expenses incurred as a result of a qualified disaster; and

- Reimburse or pay reasonable and necessary expenses incurred for the repair or rehabilitation of a personal residence or repair or replacement of its contents to the extent that the need for such repair, rehabilitation, or replacement is attributable to a qualified disaster.

The payments should not include non-essential, luxury, or decorative items or services.

Insight

Wage replacement (such as paid sick or other leave) would not be covered by Section 139, so such payments would still be taxable wages and would remain subject to income and payroll tax withholding and reporting.

Q2: What expenses might be considered to be eligible as a qualified disaster payment with respect to COVID-19?

A2: With respect to COVID-19 circumstances, it appears that employers can pay for, reimburse, or provide in-kind benefits reasonably believed by the employer to result from the COVID-19 national emergency that are not covered by insurance. For example, it appears that employers could pay for, reimburse or provide employees with tax-free payments for over-the-counter medications, hand sanitizers, home disinfectant supplies, child care or tutoring due to school closings, work-from-home expenses (like setting up a home office, increased utilities expense, higher internet costs, printer, cell phone, etc.), increased costs from unreimbursed health-related expenses and increased transportation costs due to work relocation (such as taking a taxi or ride-sharing service from home instead of using public mass transit).

Q3: What is the federal tax treatment of qualified disaster payments?

A3: Qualified disaster payments are federal tax-free to employees and are fully deductible to the employer. Such payments are not considered “gifts.” There is no federal reporting or disclosure, so such payments are not reported on Form W-2 or 1099 and are not subject to federal income or payroll tax withholding.

Q4: What is the state tax treatment of qualified disaster payments?

A4: Generally, state treatment for income tax withholding purposes will mirror the federal treatment of qualified disaster relief payments. That is, states generally exclude qualified disaster relief payments from the definition of wages for state income tax withholding purposes, either expressly or by applying the federal definition of “wages” for state income tax withholding purposes. However, qualified disaster relief payments may still be considered “wages” for purposes of state unemployment insurance tax. Employers should determine on a state-by-state basis whether certain income tax withholding and/or unemployment insurance tax contribution obligations may arise in connection with such payments.

Q5: Is there a cap on how much an employer can provide to an employee as a qualified disaster payment?

A5: No. Section 139 does not impose any limit on the amount or frequency of qualified disaster payments that an employer can make to any individual employee or to all employees in the aggregate.

Q6: Must employers have a written plan to make qualified disaster payments to employees?

A6: No. Employers are not required to have a written program for qualified disaster payments. But having such a program is recommended, so employers can inform employees about the parameters of the employer’s program in the COVID-19 context. Such a program might include a description of who is eligible, what expenses will be reimbursed (perhaps up to a “per employee” maximum), how and when payments will be made, etc.

Q7: Are employees required to substantiate their expenses to prove that they are eligible for qualified disaster payment treatment?

A7: No. Employees are not required to provide receipts or other proof supporting their expenses. However, employers could require such proof as part of its written program, perhaps using rules similar to the long-standing IRS “accountable plan” rules.

[1] COVID-19, was designated as an emergency under the Stafford Act on March 13, 2020. Although there is some debate over the legal technicalities of that declaration, it appears that Section 139 relief has been triggered. Specifically, Rev. Rul. 2003-29 says that for Section 165(i) (which is cross-referenced in Section 139), an “emergency” is treated as a “disaster.” In addition, an IRS Chief Counsel Memorandum dated June 28, 2019, states “A Federally declared disaster includes a major disaster declaration under section 401 of the Stafford Act and an emergency declaration under section 501 of the Stafford Act.”

Categories: Other Resources

Unemployment Insurance Benefits For Those Affected By COVID-19

Mar 18, 2020

The impact of COVID-19 around the United States is understandably worrisome. We’re providing this information to you regarding the latest news from the Trump administration and the State of Ohio’s unemployment benefits if you find that you have furlough all or some of your employees.

The administration also has announced this morning that the IRS will be deferring IRS payments from individuals and pass-through entities. If you owe a payment to the IRS, you can defer up to $1 million as an individual or pass-through entities and up to $10 million to corporations, interest-free and penalty-free, for 90 days.

The administration continues to work on the economic stimulus plan with Senators and House of Representatives, including loan guarantees, payments to small businesses, and payments to the American workers. After passage, they are hoping that checks to individuals can be made immediately – in the next 2 weeks.

Please rely on official sources, press conference details from national, state and local authorities, as we are, instead of media reports. We will do our best to summarize the guidelines for our clients as we understand that interpreting the messages from the CDC and Ohio Department of Health can be daunting. Besides official press conferences, our two main sources are:

- National Centers for Disease Control – Guidance for Businesses

- Ohio Business Gateway – Message to Employers

Unemployment Insurance Benefits

COVID-19 Pandemic Unemployment Payment is a new social welfare payment for employees and self-employed people who are unemployed or who have their hours of work reduced during the COVID-19 (coronavirus) pandemic. This includes people who have been put on part-time or casual work. You can apply for the payment if you are aged between 18 and 66 and have lost employment due to the coronavirus restrictions. Students can apply for the payment.

Here’s what we know as of this writing about Ohio’s unemployment insurance benefits for your employees:

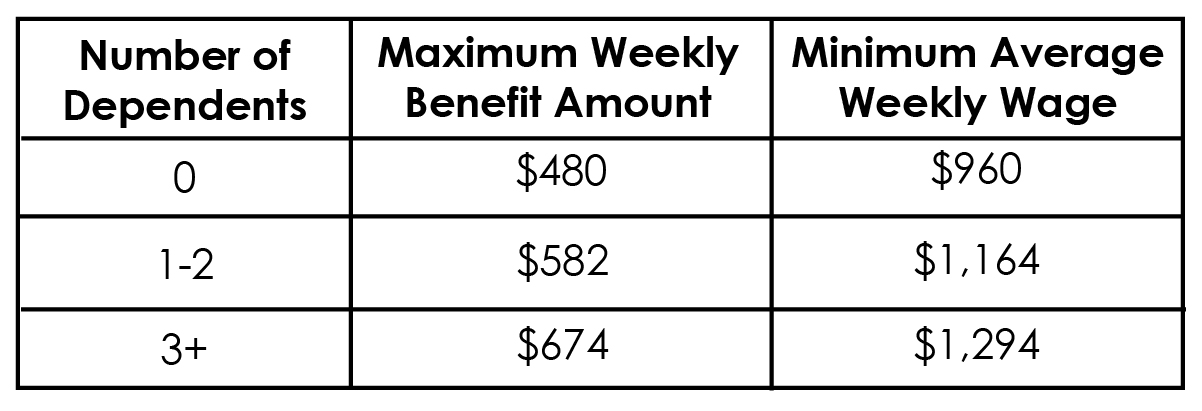

The weekly benefit amount is the amount of benefits employees may be entitled to receive for one week of total unemployment. Employees’ weekly benefit amount is computed at one-half of their average weekly wage during their base period (the base period is the 52 weeks prior to filing for unemployment). However, the weekly benefit amount cannot exceed the state’s annually established maximum levels (based on the number of allowable dependents claimed). The 2020 maximums for each dependency classification are given in the following table:

Example: $1200 average weekly wage X ½ = $600

Using this example, if an employee has 3 or more dependents, the weekly benefit amount would be $600 (as the maximum of $647 was not reached). However, if the employee had less than 3 dependents, the weekly benefit amount would be the maximum level allowable for fewer dependents (0 dependents = $480, while 1 or 2 dependents = $582).

NOTE: See below for information about deductible income and earnings which may reduce employee’s weekly benefit amount.

Employees must report all weekly income, including payments other than wages. In certain cases, the entire amount may be deducted from your benefits. Types of income that may be deductible include:

- Severance pay – Severance pay allocated by the employer to a week(s) following the date of separation is deductible from unemployment benefits.

- Vacation pay

- Pensions

- Company buy-out plans

- Workers’ Compensation

Employers can offer de minimis benefits (small amounts) like gift cards – generally under $75.

The waiting period of one week for unemployment benefits has been waived in Ohio. The Governor said employers will not be penalized for their employees filing for unemployment.

Filing for Unemployment Insurance Benefits

Ohio has two ways to file an application for Unemployment Insurance Benefits:

- Online – http://unemployment.ohio.gov – 24 hours/day, 7 days/week. Service may be limited during nightly system updating.

- Telephone – Call toll-free 1-877-644-6562 Monday through Friday 8 AM – 5 PM.

To apply for Unemployment Insurance Benefits, employees will need:

- Social Security number

- Driver’s license or state ID number

- Name, address, telephone number, and e-mail address

- Name, address, telephone number, and dates of employment with each employer worked for during the past 6 weeks of employment

- The reason why the worker has become unemployed from each employer

- Dependents’ names, Social Security numbers, and dates of birth

- If claiming dependents, their spouse’s name, Social Security number, and birth date

- Regular occupation and job skills – but employees will not have to actively search for jobs during this period.

- For your business and healthcare practices, there may be tax savings, low-interest loans through the SBA if other credit financing options are NOT available. The stimulus package being discussed is for individuals and certain small businesses under 500 employees.

Other Important Considerations

Business Interruption Insurance – Most businesses have, or should have business interruption insurance. You are urged to check with your business insurance broker to see if you have such coverage, determine if this qualifies, and what you need to do to receive reimbursement from your insurance company for your loss of business income. Up-to-date financial and payroll information will be critical.

Employment for dental workers – Healthcare workers are needed everywhere and it’s possible employees trained in HIPAA and other health safety precautions may be able to find work elsewhere. (Some requirements for HIPAA requirements have been waived for telehealth options.) Also, hospitals and medical centers are looking to dental offices to share the number of masks, gloves, etc., they have on hand.

As always, please call your William Vaughan Company advisor with any questions.

Categories: Other Resources

Unlocking the Tax Benefits of Opportunity Zones

Dec 10, 2019

Are you interested in reviving economically distressed communities in your area and reducing your tax burden at the same time? The Opportunity Zone program, created by the Tax Cuts and Jobs Act of 2017, provides the opportunity to do both.

What is an Opportunity Zone?

It is an economic development tool aimed to attract investments and jump-start economic growth in low-income urban and rural communities nationwide. To view all qualified opportunity zones, visit the U.S. Department of the Treasury for the most up-to-date listings. Zones are identified by state, county, and census tract number.

How does the program work?

It permits investors (individuals, corporations, partnerships, trusts & estates) to defer tax on any prior capital gains made from the sale or exchange of any asset, only if they invest in a Qualified Opportunity Zone (QOZ) by way of a special purpose entity known as a Qualified Opportunity Fund (QOF) within 180 days after the gain arises. In short, a QOF is an investment vehicle designed to hold funds to then invest in real estate to make “substantial improvements”.

What are the tax benefits?

- Deferral of taxable gains as late as December 31, 2026

- Qualifying investments made by December 31, 2021, and held until 2026 are eligible for a reduction in deferred gains in the amount of 10% of the gain. Investments made by December 31, 2019, and held until 2026 are eligible for an additional deferred gain reduction of 5% for a total maximum gain reduction/basis step-up of 15%.

- Permanently exempts any future gains of reinvested proceeds. Gain from appreciation in the QOF investment may be eliminated if the QOF investment is held for at least 10 years.

What should I know before investing?

Your original deferred gain (less any amount forgiven) will be subject to tax on whichever date comes first: either December 31, 2026, or when you sell your interest in an Opportunity Zone Fund. If you still own the interest in an Opportunity Zone Fund after December 31, 2026, you will owe tax on the original deferred gain without any cash proceeds from the investment to pay the tax.

When do I need to invest?

Act fast! Investing by December 31, 2019, will ensure you capture the greatest tax benefit.

Categories: Tax Planning