{kind=link}

A time of reflection

Dec 26, 2013

I hope everyone had a wonderful holiday celebrating with friends and family. The holidays can be an exciting time but also can be stressful and difficult for many people. I’ve heard stories recently of tragic events, but also there are some great stories out there about some really great people. I am sure by now you have heard about the WestJet airlines present give away. If you haven’t seen the video it is a must see. Just shows there are still some really great people out there. Also there was a local story in my area about some good guys who saved Christmas for a family’s whose home with their Christmas presents was unreachable due to flooding. Sadly there were stories of accidents and tragedy as well, which are never easy, but are all too difficult at Christmas. There are families who are separated by miles who cannot spend the holiday’s together and there are families close by that choose to stay apart. I wish all reading this a wonderful remainder of 2013.

It is easy to reflect on our personal life and think about everything we wished we had done, or even that we hadn’t, but do we include our work life in that? Are there things at our job that need to be improved upon or things that we keep putting off? Do we say maybe next year?

Maybe your operations are not quite as smooth as you would like them to be. Each person basically knows what their job is, but no one else quite knows what anyone else is doing, and many tasks seem to either overlap or get missed altogether. Wouldn’t it be nice to have an organized manual that directs each person as to what their role is and allows anyone to quickly fill another’s shoes-keeping your operations running smoothly? If you answered yes to that, then maybe it’s time for an operations review!

Or maybe it’s your costing figures. You’ve known for a while that your numbers just cannot be right and that they are not reliable at all, but you’ll get to that later. Stop making bad decisions because you do not have good information.

Another big issue I often see is an outdated or unusable software system. Does everyone have their own Excel spreadsheet calculating something a little bit differently because no one is using the software system? It’s time to get the necessary training to use your system correctly, or to get a better system.

Whatever is necessary now is the time to make the changes to make 2014 the best year ever. Remember you do not have to do it alone either, just have to admit it needs to be done and see that it gets done!

Categories: Cost Accounting

The Dreaded “B” Word – Budget

Dec 19, 2013

2013 has almost come to a close and 2014 is not just knocking, but pounding on the door now. You may be tempted to say it’s too late to start a budget now, but I’m here to tell you it’s not!

If you have been out shopping lately or even just driving around you will notice there are a lot of procrastinators out there. Some people just wait until the very last minute, while others are trying to get the best deals. Regardless, it can be quite hectic, but doesn’t mean it’s impossible to do. Just may take a little extra effort. The same somewhat holds true when it comes to creating a budget. If you have not done your budget yet, I’m going to take a wild guess and suggest you are one of those last minute shoppers out there too!

If you have been out shopping lately or even just driving around you will notice there are a lot of procrastinators out there. Some people just wait until the very last minute, while others are trying to get the best deals. Regardless, it can be quite hectic, but doesn’t mean it’s impossible to do. Just may take a little extra effort. The same somewhat holds true when it comes to creating a budget. If you have not done your budget yet, I’m going to take a wild guess and suggest you are one of those last minute shoppers out there too!

It will take a lot of effort to get everything together in short order, but I feel it is quite necessary! You need to pull all of the departments together to get the necessary information and hold others accountable. Set firm deadlines and stick to them! It is important to analyze the budget and make sure that it is reasonable. Do not just put numbers in a spreadsheet just for the sake of doing it. It is important that you look at past trends and future contracts when setting your budget.

If you do not have a budget for 2014 then how will you know how you are doing? Are you hitting your targets? Do you need to try to cut costs, or increase revenues? Are your costing standards accurate and reasonable? If you do not know what it is supposed to be, how do you know what is-is accurate?

Do not use the fact that 2013 is almost over as an excuse to not do a 2014 budget. Get in gear and do it today! Oh yeah and I said it….BUDGET!

Categories: Cost Accounting

What Is The Primary Reason To Understand Your Product Cost?

Dec 16, 2013

I can answer that with one succinct statement: knowing your product cost is not so important for setting a price as it is to manage your costs for operational purposes.

Cost based pricing has many advantages (assuming you know your costs), it’s flexible, easy to calculate and change, and its very transparent. It also has many disadvantages, it ignores competition and to a large part product demand, it forces price increases and decreases if your costs change, and most importantly, it doesn’t provide any incentive to improve your cost efficiency.

In my opinion, the disadvantages far outweigh the advantages. The most important factor in setting the sales price is the sales demand as a function of your price. This demand is influenced by competitor’s prices, customer preferences, and the availability of an equivalent product from another supplier.

What does all this mean? For most of my clients, the price they can charge is dictated by the market. So, knowing product cost is crucial to their success because they have to manage their costs to be profitable.

What does all this mean? For most of my clients, the price they can charge is dictated by the market. So, knowing product cost is crucial to their success because they have to manage their costs to be profitable.

So many sales decisions have to be made based on COST. Occasionally you are faced with a sales opportunity for which only incremental costs and revenues for that one transaction are relevant. Then there are intermediate or long-term decisions which include more than incremental costs such as fixed costs the company is incurring.

In the long run, it’s pretty simple! The revenues of the company must exceed its costs to survive. If your cost is set by the market, then there is only one variable you can change: YOUR COST! The management accounting system needs to provide information to the managers about whether sales prices for products are in excess of their FULL cost of production to provide the company with a sufficient rate of return. If we are not covering the full product cost, then managers need to be equipped to make those hard decisions such as dropping products that are unable to cover their full costs.

Experience has shown that if you go to the operations team and are precise about what the problem is then they can fix it. “Precise” meaning they need to take three cents out of material cost for every unit produced, not we need to reduce the product cost.

If the team is not able to deliver the required reductions in cost and our system supports that, it is time to re-evaluate this sale. There may be extenuating circumstances that would lead you NOT to eliminate this product, but you will not be able to make that decision without sufficient costing information!

Categories: Cost Accounting

Marginal Costing & Its Application

Dec 13, 2013

Recently I was talking to a CFO concerning costing methods that might work in his manufacturing plan. We talked about a number of systems and he brought up marginal costing.

This CFO was relatively inexperienced in manufacturing and very inexperienced in various job costing methods. As a result, when he asked about marginal costing, I presume this was from some conversation he had with one of his colleagues or something in which he had read. In any event, he began the discussion with a statement that he thought marginal costing was a stand alone costing method and mutually exclusive of any other method.

I have used marginal costing techniques with other clients, but never as a stand alone process that is not supported by a complete costing system including full absorption techniques on a part of the system. The reason is very simple, most companies cannot afford and would not want to use multiple costing systems to do significantly different functions in their operation. For example, for inventory valuation purposes both GAAP and income tax have costing methods that include full absorption concepts although they might be different from each other, they both have requirements that include recognition of differing sets of overhead.

It is common to need marginal costing techniques for certain components of management needs as opportunities or problems present themselves. In my past experience, if a company is thinking about their options they will require some time in the future as they design their costing model. This way they can build in certain options to allow products to be costed in several different ways including marginal costing. This would allow for a company to do an analysis of one or more of its product lines in addition to extracting cost from its cost system relative to those products on a marginal costing concept.

If the next problem to be addressed includes analysis of complete product cost including full absorption, then the same cost model can be queried in another way to provide full absorption costing on the same exact products.

Depending on the complexity of the manufacturing processes, the number of products in inventory and the complexity of the cost band associated with each product, this analysis can be relatively simple or very complex.

The end result of our conversation was that his current cost model may well have the capabilities to do this analysis and he was going to spend some time to delve into more of the reporting capabilities of his system and how the cost bands were configured to see if this marginal costing analysis is possible.

Categories: Cost Accounting

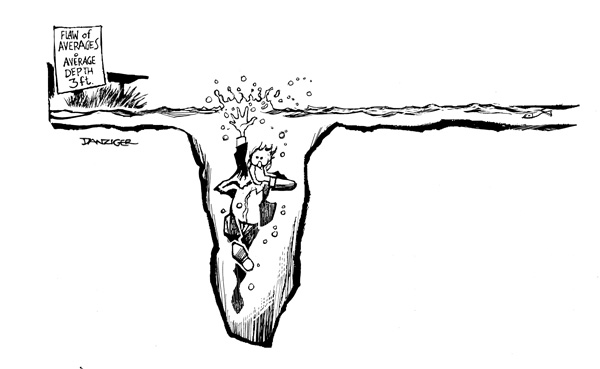

The Flaws of Averages: How Not To Model Your Cost System

Dec 09, 2013

I was in a meeting last week with a potential costing client when I heard a saying that I had never come across before: “have you ever heard the story of the army that drowned in a river that was an average of three feet deep?”

Of course I came back to the office and googled it to find the source, and here is what I came up with: http://flawofaverages.com/FOA%20Highlights/Highlights7%20F4.1.htm

According to Mr. Sam Savage, it’s not an army but a group of statisticians. Of course! In case you are still lost, the overriding theme here is that you cannot effectively manage your Company if you are using grand averages to tell you what you need to know. For this group of statisticians, the first part of the river was shallow, and the other part of the river was deep which resulted in a grand average of three feet which is manageable!

According to Mr. Sam Savage, it’s not an army but a group of statisticians. Of course! In case you are still lost, the overriding theme here is that you cannot effectively manage your Company if you are using grand averages to tell you what you need to know. For this group of statisticians, the first part of the river was shallow, and the other part of the river was deep which resulted in a grand average of three feet which is manageable!

Apply this to the costing world. Most of the Companies that I am called to are in the following position(s):

- Monthly financial statements that show an overall profit or loss and are often inaccurate

- Lack of systems or utilization of systems that does not provide essential information

- Little or no detail of product cost by product/ customer/ territory/ or other segment

- If there is detail, it is often very misleading and does not reconcile to anything and is generally based on a foundation of misunderstood work centers, allocation theories that missed the boat, and sometimes a disassociation from the reality of how resources are truly being consumed.

So, decisions are being made using the profit and loss statement each month. What good does that overall gross profit margin tell you? Assuming you have done a good job of correctly identifying your costs, it gives you a GRAND AVERAGE which is pretty much useless if you want to make effective decisions for the future strategy of your company.

- Do you know which product or family of products is causing your gross margin to increase?

- Do you know which product or family of products is losing money causing your overall grand average to be lower?

- Do you know which “losing” jobs are ok to maintain because they are part of an overall “winning” group to a customer?

- Can that grand average profit margin tell you which customer or product to “cut loose”?

In case you haven’t said it already, I will do it for you. NO, that grand average cannot give you any of those answers. If you can associate with any part of this scenario, then your company is not operating at its maximum potential. It is time to implement a new costing theory that is transparent, accurate, built on solid facts and assumptions, and provides results that will identify and understand WHAT is driving your overall grand average.

Categories: Cost Accounting